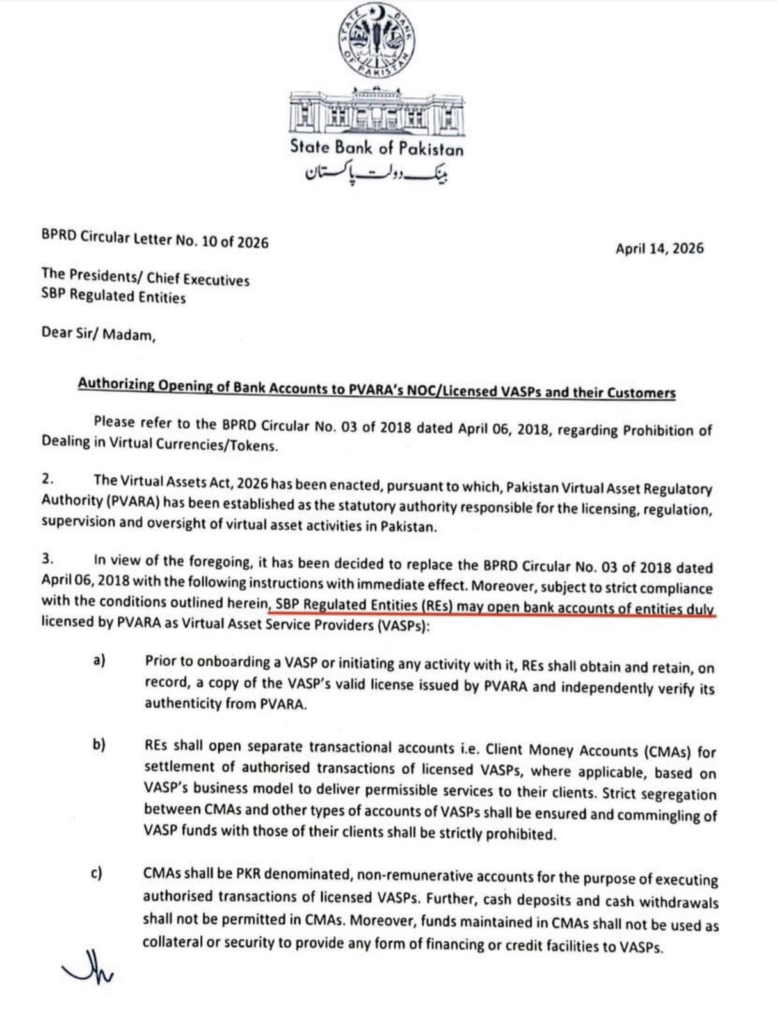

Islamabad :In a landmark regulatory shift, the State Bank of Pakistan (SBP) has permitted Virtual Asset Service Providers to open formal bank accounts, effectively ending an eight-year prohibition that isolated the nation’s crypto sector from the traditional financial system. This pivotal decision, reported by Reuters in early 2025, represents a calculated move toward integrating digital assets into Pakistan’s economic framework while establishing crucial oversight mechanisms.

Pakistan Crypto Regulation Enters a New Era

The State Bank of Pakistan issued new guidelines that fundamentally alter the banking landscape for cryptocurrency businesses. Consequently, licensed Virtual Asset Service Providers can now establish banking relationships after presenting their government-issued VASP licenses for verification. However, the central bank simultaneously imposed strict limitations on traditional financial institutions. Specifically, banks cannot invest customer deposits in cryptocurrencies or hold such digital assets on their balance sheets. This dual approach aims to foster innovation while containing systemic risk.

Previously, Pakistan maintained a restrictive stance toward cryptocurrencies since 2018. The Financial Action Task Force (FATF) repeatedly urged the country to regulate virtual assets to combat money laundering and terrorist financing. Therefore, this regulatory evolution aligns Pakistan with international standards. Moreover, the nation’s significant remittance inflows and large unbanked population create a practical use case for regulated crypto services. Industry analysts immediately recognized the move as a strategic step toward formalizing a previously opaque sector.

Understanding the New VASP Framework

The term Virtual Asset Service Provider encompasses a range of cryptocurrency businesses. Under the new State Bank of Pakistan rules, these entities must obtain official licenses before approaching banks. The regulatory framework categorizes VASPs clearly:

- Crypto Exchanges: Platforms facilitating the trading of digital assets.

- Custodial Wallet Providers: Services holding private keys on behalf of users.

- Digital Asset Brokers: Intermediaries executing trades for clients.

- Initial Coin Offering Platforms: Entities facilitating token sales.

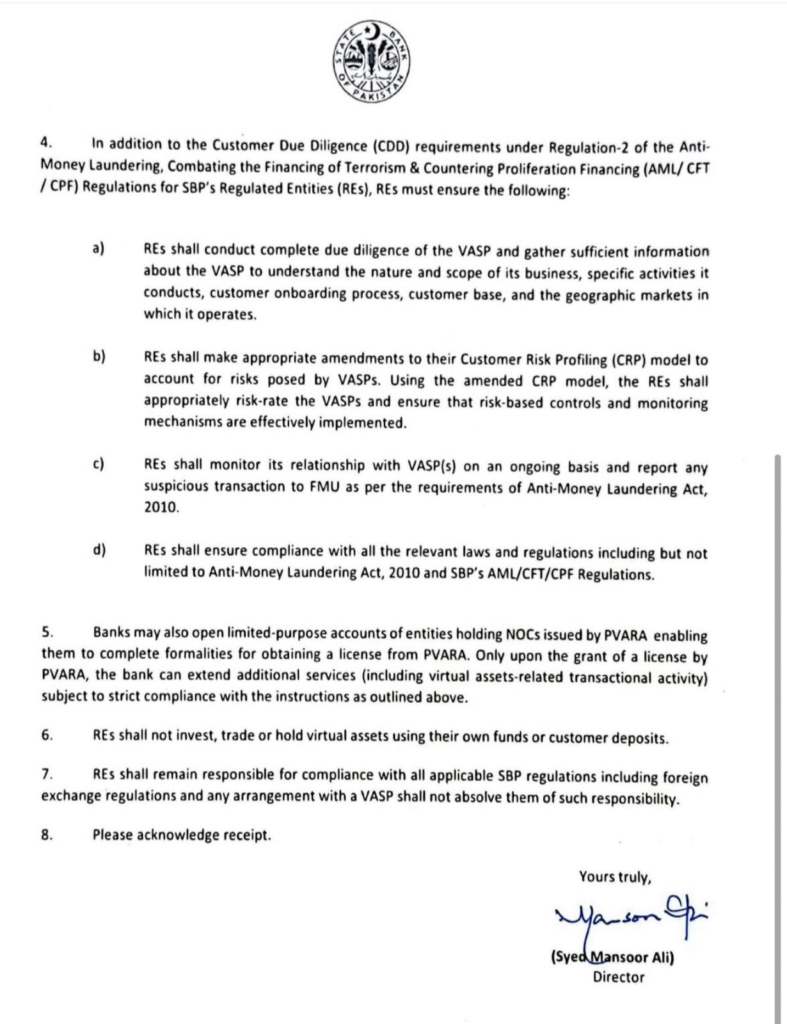

Banks must conduct enhanced due diligence on all VASP clients. This process includes verifying the authenticity of licenses with relevant government agencies. Furthermore, financial institutions must monitor VASP transactions for suspicious activity continuously. The central bank mandates regular reporting on these banking relationships. This structured approach provides a compliance pathway for legitimate operators while filtering out unlicensed entities.

Comparative Analysis: Pakistan’s Regulatory Position

Pakistan’s new stance places it within a growing cohort of nations establishing clear crypto banking rules. The following table contrasts Pakistan’s approach with regional counterparts:

Country Bank Account Access for Crypto Firms Licensing Requirement Bank Investment in Crypto Pakistan (2025) Permitted for licensed VASPs Mandatory Government License Prohibited India Restricted, subject to case-by-case review Registration with Regulatory Authority Not Permitted United Arab Emirates Fully Permitted in Special Zones Free Zone or Central Bank License Allowed under Specific Rules Bangladesh Generally Prohibited No Formal Framework Banned

This comparative view illustrates Pakistan’s middle-ground strategy. The nation avoids an outright ban but implements stronger safeguards than some progressive jurisdictions. Importantly, the policy acknowledges the economic reality of crypto adoption while prioritizing financial stability.

The Economic and Technological Impact

The decision carries significant implications for Pakistan’s economy and technological development. Firstly, it provides a legitimate channel for billions in remittances. The World Bank estimates Pakistan received over $24 billion in remittances in 2023. Crypto corridors potentially offer faster, cheaper transfer methods. Secondly, the move could attract foreign investment in fintech. International crypto exchanges may now consider entering the Pakistani market through licensed local partnerships.

Technologically, integration with the banking system validates blockchain innovation. Pakistani developers can now build financial products with clearer regulatory guidance. Additionally, the requirement for government licenses creates a formal registry of operators. This registry enhances consumer protection and tax compliance. The central bank’s cautious approach reflects lessons from volatile markets elsewhere. By prohibiting banks from direct crypto exposure, Pakistan insulates its traditional financial system from asset price swings.

Historical Context: From Ban to Regulation

The eight-year journey to this point involved several key phases. In 2018, the State Bank of Pakistan effectively banned banks from dealing with cryptocurrencies. This prohibition responded to FATF concerns and domestic volatility fears. Subsequently, a 2021 government study committee recommended a regulated framework instead of a blanket ban. Then, in 2023, Pakistan passed initial legislation defining virtual assets and service providers. The 2025 banking access rules operationalize that earlier legislation. This timeline shows a deliberate, staged approach to policy development.

Operational Challenges and Compliance Requirements

Implementing the new framework presents practical challenges for both banks and VASPs. Financial institutions must train staff to identify legitimate licenses and monitor crypto-related transactions. They need to develop new risk models for VASP clients. Conversely, VASPs must navigate a potentially complex licensing process with multiple government agencies. They also face ongoing reporting obligations to maintain their banking access.

Key compliance pillars under the State Bank of Pakistan guidelines include:

- Anti-Money Laundering Checks: VASPs must implement robust AML protocols matching banking standards.

- Transaction Monitoring: Real-time tracking of fund flows to flag unusual patterns.

- Capital Requirements: Minimum capital thresholds for licensed VASPs to ensure operational stability.

- Consumer Disclosure: Clear communication of risks to cryptocurrency customers.

These requirements aim to build a transparent ecosystem. Successful implementation could position Pakistan as a regional model for balanced crypto regulation.

Conclusion

The State Bank of Pakistan’s decision to allow bank accounts for licensed Virtual Asset Service Providers marks a transformative moment in the nation’s financial history. This policy shift ends an eight-year isolation of the crypto sector and initiates a regulated integration phase. While maintaining prudent safeguards, particularly prohibiting banks from direct crypto investment, the framework acknowledges digital assets’ economic potential. The move aligns Pakistan with global regulatory trends and addresses longstanding FATF recommendations. Ultimately, this Pakistan crypto regulation breakthrough could enhance financial inclusion, modernize remittance channels, and stimulate responsible fintech innovation. The coming months will test the implementation’s effectiveness in balancing innovation with stability.

FAQs

Q1: What exactly has the State Bank of Pakistan changed regarding crypto firms? The State Bank of Pakistan now permits licensed Virtual Asset Service Providers to open and maintain formal bank accounts. This reverses an eight-year prohibition that prevented crypto businesses from accessing the traditional banking system.

Q2: Can Pakistani banks now invest in or hold cryptocurrencies? No. The new rules explicitly prohibit banks from investing customer funds in cryptocurrencies or holding such digital assets on their own balance sheets. The banking access is strictly for servicing licensed VASP clients, not for direct crypto exposure.

Q3: What is a VASP, and who needs a license? A Virtual Asset Service Provider includes cryptocurrency exchanges, custodial wallet services, digital asset brokers, and ICO platforms. Any entity conducting these activities for Pakistani customers must obtain a government-issued VASP license to qualify for bank account access.

Q4: How does this affect ordinary cryptocurrency users in Pakistan? Ordinary users should benefit from increased security and legitimacy. They can now use licensed platforms that operate with banking oversight, potentially offering better consumer protection. However, personal crypto holdings are not directly affected by these commercial banking rules.

Q5: Why did Pakistan make this change after eight years? The change responds to international regulatory pressure, particularly from the FATF, and domestic economic needs. It aims to formalize a growing sector, enhance oversight of crypto transactions, and potentially leverage blockchain technology for financial inclusion and remittance efficiency.

This post Pakistan Crypto Regulation Breakthrough: Central Bank Lifts 8-Year Ban on VASP Bank Accounts first appeared on BitcoinWorld.